Contact

ContactThe Human Capital Factor: Employee Motivation and Its Implications for Investing

May 01, 2023-

Human capital is a crucial intangible asset: difficult to measure, yet critical to company success

-

Harbor's suite of human capital ETFs are based on new, proprietary data measuring companies’ Human Capital Factor

-

The ETFs capitalize on an accounting inefficiency and company trends not captured elsewhere, offering exciting new potential sources of alpha

-

The ETFs follow a clear investment process, backed by strong behavioral-economics research

The majority of corporate value increasingly resides in intangible assets. In our view, human capital is without doubt one of the most critical of these assets, encompassing the habits, knowledge, talent, motivation, and experiences of an organization. Until now, lack of robust, standardized data limited investors’ ability to integrate these intangibles into company valuations, leading to their potential undervaluation by the market. We believe, through sound and differentiated behavioral economic research, investment research firm Irrational Capital has uncovered a potential new source of alpha and direct link between company culture and equity performance – the Human Capital Factor (HCF).

The HCF is a breakthrough in discerning which companies manage their human capital well and how that may translate into outperformance. Harbor Capital now offers a suite of ETFs that capture this newfound value by tracking indexes that favor companies with strong Human Capital Factor scores.

Here, we lay out why we believe companies that successfully manage their human capital are wellpositioned to achieve long-term equity outperformance.

Investment Thesis:

-

A skilled, motivated workforce contributes materially to improved company performance

-

Accounting rules currently treat human capital as an expense or future liability, not an asset

-

When accounting rules fail to represent the economic reality, an equity mispricing can emerge, creating opportunities for investors

-

New data measuring the Human Capital Factor provides a new potential source of alpha

Managers routinely say: “People are our greatest asset,” acknowledging the importance of human capital and corporate culture. However, accounting rules generally treat human capital as an expense or future liability rather than an asset.

Two ways compete to explain this gap between what most companies say about the importance of their people and how they classify investments in human capital:

-

Curtain-dressing: companies are not all that interested in human capital, yet executives feel obliged to say the right thing to their employees.

-

A measurement problem: companies would like to account differently for human capital, but measuring it is more complex than measuring other company assets and lacks clear guidelines. As a result, most companies fail to measure – and optimize for – human capital factors.

By collecting a rich, proprietary dataset, Irrational Capital has been able to systematically measure and quantify the Human Capital Factor (HCF) – a company’s ability to create economic value derived from its workforce’s habits, knowledge, talent, motivation, experience, and attributes.

The alternative data establishes a relationship between employee motivation and the impact on a company’s stock price. In the following pages, we present information supporting the argument that companies with the ability to better manage human capital have the potential to achieve long-term equity outperformance.

What is the Human Capital Factor?

-

A new quantitative investment factor by scientifically measuring what has historically been subjective and qualitative, i.e., how do employees feel and how motivated are they?

-

Behavioral research shows workforce productivity is highly dependent on intrinsic motivation

-

A new approach to quantifying a company’s human capital that seeks to access undiscovered sources of equity mispricing

Behavior Fuels the Human Capital Factor:

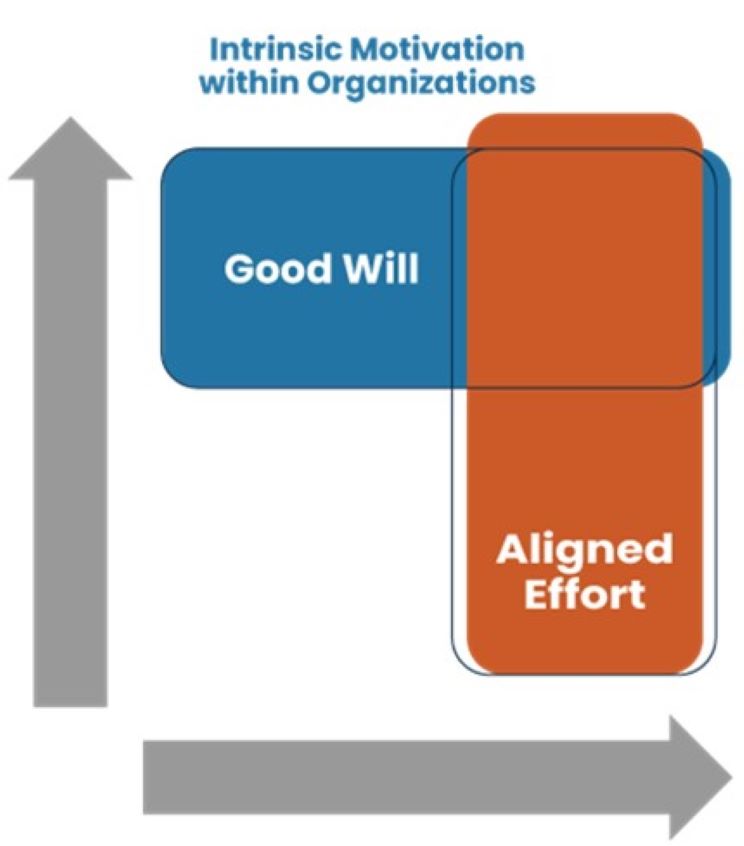

To understand how people behave in the workplace, it is critical to understand why employees choose to act one way over another. Workforce motivation plays an outsized role in how effectively employee resources are deployed.

Broadly, two forms of motivation exist: Extrinsic and Intrinsic. Extrinsic motivation is driven by factors such as financial compensation, benefits, job title, and physical environment. By contrast, intrinsic motivation is determined by factors such as autonomy, feeling appreciated, having a sense of purpose or alignment on a greater mission. In some respects, it’s easier to quantify factors influencing extrinsic motivation. However, a substantial and growing body of behavioral research shows employee performance is highly dependent on intrinsic motivation. What matters is emotional, personal, and difficult to quantify.

For this reason, intrinsic motivation may lead to material sources of mispricing in company valuations. Those who can effectively measure the factors driving intrinsic motivation stand to gain a fresh perspective on a company’s ability to create and capture value.

Value creation through the Human Capital Factor:

How do we quantify something as intangible as workforce motivation and link it to tangible company performance? Irrational Capital set out to answer that question through extensive academic research, which resulted in the development of the Human Capital Factor (HCF).

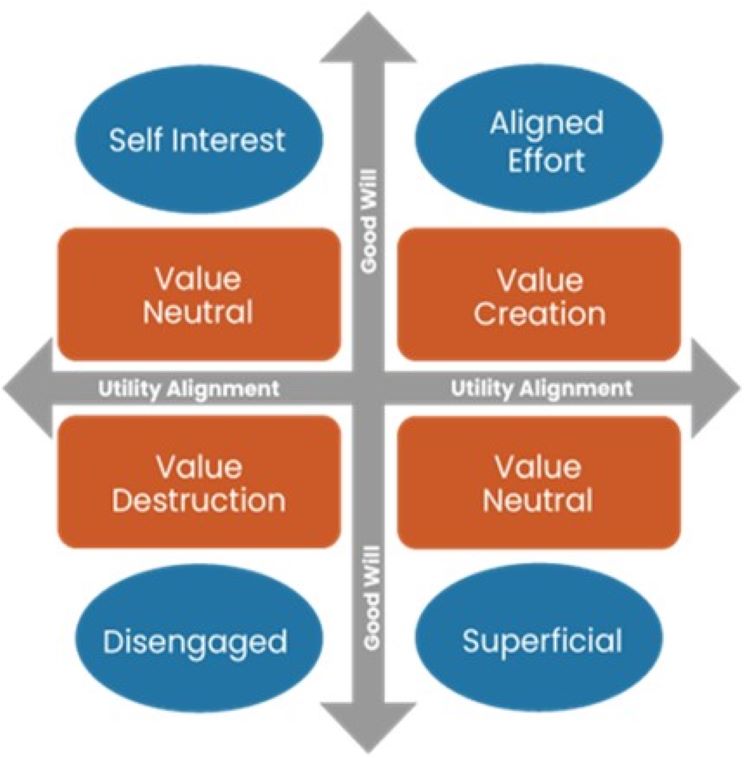

The HCF considers two ways in which motivation influences company success – Good Will, which quantifies employee effort, and Utility Alignment, which quantifies how engaged employees are with the company’s goals.

Disengaged employees who exert little effort and are less invested in broader goals destroy value. That said, extra effort without benefits to the company, or working towards company goals without an exertion of one’s best effort are Value Neutral, at best.

Conversely, employees with an elevated level of Good Will towards the employer are more likely to expend extra effort in the workplace. Employees with a high level of Utility Alignment would be more likely to expend that effort so that it benefits the organization as a whole (rather than limiting focus strictly to job requirements or to self-serving efforts.)

The Twin Pillars – Good Will and Utility Alignment:

These two crucial building blocks for the HCF – Good Will and Utility Alignment – provide a way to link workforce motivation to company performance.

Good Will is captured in the range between the minimal effort someone needs to produce in order not to lose their job and the maximum effort someone can produce if they are truly and fully engaged in what they are doing.

Multiple behavioral experiments have shown strong evidence for non-monetary influence on an employee’s Good Will range. Intrinsic motivation factors have repeatedly correlated with meaningful productivity increases1,2.

Utility Alignment represents the willingness and desire of the employee to take on tasks that are in the best interest of the company (and, consequently, its stakeholders, including shareholders).

1 (Ryan & Deci, Intrinsic and Extrinsic Motivations: Classic Definitions and New Directions, 2000)

2 (Ryan & Deci, Self-Determination Theory and the Facilitation of Intrinsic Motivation, Social Development, and Well- being, 2000)

Crucially, Utility Alignment isn’t simply measuring happiness or satisfaction. Indeed, when individuals engage in Utility Alignment tasks, they often do this at the expense of completing their own tasks or undertaking activities outside of work.

Companies can – and do – have very different approaches to cultivating intrinsic motivation:

-

Some companies provide feedback; others attempt to control behavior

-

Some foster an open dialogue with direct managers; others codify a strict hierarchy

-

Some help employees develop skills and support autonomy; others maintain rigid role specifications

In short, companies that effectively support intrinsic motivation factors would score highly on both Good Will and Utility Alignment than others. Until now, investors couldn’t capture these choices into their assessment of companies, nor could they compare different companies’ performance on these factors.

Differentiated Data:

To consistently evaluate behavioral patterns within and across firms, self-reported assessments have been shown to be the most valid, genuine approach to collecting data about individual perceptions and wellbeing.

Irrational Capital has built a robust data universe comprised of employee feedback. The data universe contains employee feedback from several sources including:

-

Publicly available data sources, including crowdsourced employee feedback from employer review sites (i.e., Glassdoor) with over 12 years of continuous data across several categories of well-being and organizational characteristics.

-

Proprietary data including over 15 years of line-item employee well-being self-reported data from employer-sponsored assessments regarding the employee-employer relationship, from multiple survey companies.3

The entirety of the combined data sets in Irrational Capital’s research universe contains over 4,700 public companies, more than 15 million individual employee respondents, and over 700 million data points, including a range of self-reported demographic characteristics (such as gender, salary-band, seniority level, tenure, and more).

The team at Irrational Capital constantly searches for new, robust data sources in order to continually improve and expand its universe. Most recently, they researched and implemented new data sources to increase the breadth of coverage for small cap companies. In addition, research is ongoing on international datasets that will allow them to broaden their coverage globally.

The data maps into seven key dimensions (see below for category definitions). Combined, these behavioral traits seek to capture how companies treat their employees and how the employees perceive their company.

3 The proprietary data sets have never been used for investment purposes prior to Irrational Capital’s acquisition of data, and the data is exclusive to Irrational Capital for investment purposes. We believe this is largest assembled collection of data on the topic of human capital management.

|

7 dimensions |

Description |

|

|---|---|---|

|

Direct Management |

⟶ |

Employees' satisfcation on direct manager support and help for learning and growth |

|

Organizational Alignment |

⟶ |

Employees' feeling on how much they are informed and aligned to the direction, goal and value of the organization |

|

Engagement |

⟶ |

Employees' enthusiasm and absorbedness about their work and willingness to take positive action to further the organization's reputation and interests |

|

Innovation |

⟶ |

Employees' feeling on how organization encourages new and creative ideas, processes, products |

|

Organizational Effectiveness |

⟶ |

Employees' feeling on how effective the organization has achieved intended outcomes through cooperation, training et. |

|

Emotional Connection |

⟶ |

Employees' bonding with organization and feelings with workplace |

|

Extrinsic |

⟶ |

Employees' satisfaction on organization outside rewards such as the pay, benefit package and work life flexibility |

Utilizing this schema, Irrational Capital would expect to find that queries related to themes in the Extrinsic category will matter less to future equity performance than queries related to the Intrinsic Motivational themes (all the other categories).

Harbor's Suite of Human Capital ETFs

-

Provides an objective and systematic way to invest in companies that best manage human capital based on Irrational Capital’s proprietary methodology

-

Offers exposure to companies with high Human Capital Factor scores in each ETF’s respective universe

-

Is grounded in robust behavioral science research and backed by robust data sets

-

Offers a compelling way to invest in the S of ESG4 (Environmental, Social, and Governance), which tends to be underrepresented in sustainable investing and beyond

Harbor presently offers a suite of three ETFs that offer investors a way to benefit from the Irrational Capital’s research on the Human Capital Factor.

Harbor Corporate Culture ETF (HAPI) provides exposure to large-cap companies with high HCF scores. Its portfolio is broadly diversified and sector neutral.

Harbor Corporate Culture Leaders Factor ETF (HAPY) provides unconstrained, equally weighted exposure to companies with high HCF scores across the market-cap spectrum (with a large cap bias).

4 Framework designed to be embedded into an organization's strategy that considers the needs and ways in which to generate value for all organizational stakeholders.

Harbor Corporate Culture Small Cap ETF (HAPS) provides broadly diversified, sector neutral, exposure to small cap companies with high HCF scores.

The table below provides key characteristics for each ETF as of 3/31/23:

|

HAPI |

HAPY |

HAPS |

|

|---|---|---|---|

|

Underlying Index |

CIBC Human Capital Index |

Human Capital Factor Unconstrained Index |

CIBC Human Capital Factor Small Cap Index |

|

Morningstar Category |

Large Blend |

Mid-Cap Growth |

Small Blend |

|

Number of Holdings |

100-150 |

70-100 |

200 |

|

Approx % in Top 10 Holdings |

30-35% |

10-20% |

25-30% |

|

Minimum market cap |

$11 billion |

$1 billion |

$1 billion |

|

Sector Neutral |

Yes |

No |

Yes |

|

Position Size Limit |

5% |

Equally weighted |

2% |

|

Expense Ratio |

0.36 |

0.50 |

0.64 |

Harbor believes this range of products provides investors with tools to incorporate a potentially new investment factor in ways that make sense for their portfolios.

Human Capital as an Asset – Secular Trends

The Rise of Intangibles |

Socially Aware Investing |

Labor Dynamics |

Demographic Changes |

|---|

At its core, the HCF research contends that a motivated workforce is a valuable, intangible company asset. We believe companies with the ability to better manage human capital have the potential to achieve equity outperformance over time.

Four long-term secular trends support our view. First is the consistent rise in intangibles as a proportion of companies’ book value5. Second, the rise of ESG/Diversity, Equity and Inclusion (DEI) and the push for socially aware stakeholder engagement. Third, various labor dynamics including the shift to hybrid work, which has become entrenched since the COVID-19 pandemic. Finally, longstanding demographic changes, resulting in an aging workforce and growing skills scarcity.

Each of these trends separately underlines the role of the Human Capital Factor in company valuations. Combined, they show how ignoring it may lead to substantial equity mispricing.

5 an accounting term used for both a measure of a business's equity and the value of an asset as it appears on a balance sheet. In the case of a business, book value is usually calculated as part of a sale, investment decision or liquidation of the business.

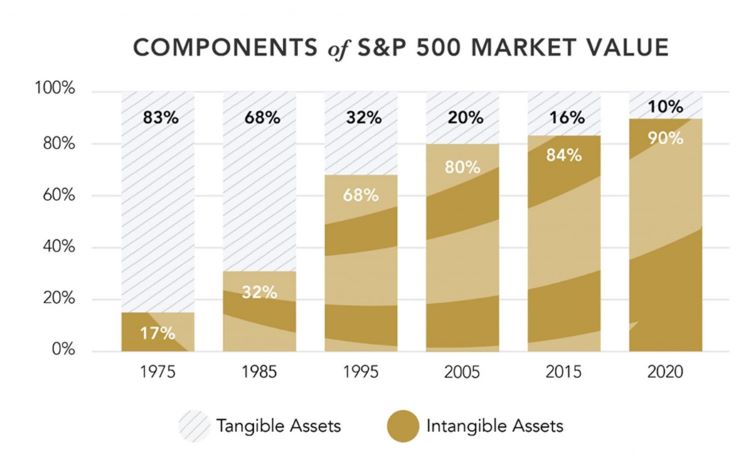

Trend 1: The Rise of Intangibles

The market derives much of its information from company financial statements, which are compiled according to accounting standards (such as the GAAP - Generally Accepted Accounting Principles). However, intangible assets – for example, intellectual property – have become critical in the knowledge economy but are not quantified as assets, according to current reporting standards. Nevertheless, intangible assets can have meaningful impact on company value.

According to research from Ocean Tomo, intangible assets represented 90% of the market value of the S&P 500 Index as of 2020. (Intangible Asset Market Value Study, 2020)i

When accounting rules fail to represent economic reality, equity mispricing can emerge, potentially providing a new avenue for alpha creation. Although corporate culture doesn’t appear as a line on the balance sheet, it is an important intangible asset that adds to a company’s worth. The HCF introduces a new way to measure to distinguish between companies with a great corporate culture from those with a toxic or dysfunctional one.

Trend 2: Socially Aware Investing

Investors’ increased focus on companies’ environmental, social, and governance (ESG) strategies represents a shift in thinking away from shareholder capitalism toward stakeholder capitalism, where benefits are aligned for shareholders, employees, and society at large. The shift toward stakeholder capitalism is further evidenced by the broad uptake of Diversity, Equity & Inclusion (DEI) policies by companies across the globe. According to a 2022 global DEI survey by PWC, 85% of companies responding said that DEI is a stated value or priority. (Diversity, Equity & Inclusion Benchmarking Survey, 2022)ii

The tilt towards environmental investing, which is now in full force, has led to a wealth of environmental data for benchmarking purposes. More recently, the rise of socially-aware investing pushes investors to seek data capturing a company’s ability to build a diverse and inclusive workforce and to manage its human capital fairly.

However, beyond the florid self-penned essays in companies’ annual reports, investors have had little concrete evidence, let alone sufficiently standardized and detailed data, to allow for comparisons between companies. We believe the HCF offers a differentiated, comprehensive measure of corporate social performance.

Trend 3: Labor Dynamics and The Shift to Hybrid Work Environment

Even prior to the Covid-19 pandemic, technological innovation was making remote work feasible for a growing portion of knowledge-economy employees. The pandemic hastened the transition, and hybrid work environments have become fully entrenched in the post-pandemic world.

A 2022 Gallup survey found that 8 in10 employees in the US are working hybrid or fully remote. Positions with hybrid schedules in the US are expected to grow from 42% in 2021 to 84% in 2024, according to an AT&T study. (The 2022 Status Of Remote Work And Top Future Predictions, 2022)iii

Employees have expressed a clear desire to keep the hybrid model. For example, a 2022 survey from Korn Ferry found that 49% of professional respondents would turn down a job offer if the company mandated they go into the office full time. (Future of Work Trends 2022, 2022)iv Similarly, a Gartner survey in 2002 found that 43% of employees said that they would seek other jobs if their employers required them to return to the office. (Future of Work Reinvented, 2023)v

However, employers are not as enthusiastic about the hybrid models, bringing about a new source of friction. A 2022 Microsoft survey found a significant difference in perception between employees and employers regarding productivity in hybrid work environments. (Hybrid Work Is Just Work. Are We Doing It Wrong?, 2022)vi

By measuring factors such as autonomy and trust, the HCF provides a quantifiable way to distinguish companies that will flourish in the hybrid-workplace era.

Trend 4: Demographic Changes

Birthrates are falling across all major economies. The birth-rates of the United States, the United Kingdom, Japan, Germany, France, and South Korea – all lie below the ‘replacement rate.’

These demographic changes are resulting in an aging population and an ever-tightening labor market. According to data from the U.S. Bureau of Labor Statistics (BLS), the share of workers aged 55 and older has grown from 13% in 2000 to 23% in 2021, and the BLS expects the percentage to reach 25% by 2031. (The Number of Older Workers Is Growing Quickly as They Continue to Face Economic Challenges, 2022)viii What’s more, the U.S. Labor Department expects this age cohort to take roughly half of all jobs created over the next decade. (The Over-55 Crowd Is Key to U.S. Workforce Growth. So Is the Over-75 Crowd., 2022)ix

How companies navigate these demographic changes will greatly influence their competitive position. Growing skills scarcity spells out success for companies able to retain and attract talent. Equally, a company’s capacity to upskill its workforce will enable it to continue benefiting from aging employees’ expertise. The HCF’s systematic assessment of engagement and organizational effectiveness helps point to companies with the capacity to effectively manage changing workplace demographics.

-

We believe human capital is a crucial intangible asset and a potential driver of equity performance

-

Secular trends such as the rise of intangibles, socially aware investing, the shift to hybrid work models and demographic changes highlight the growing importance of human capital management to company success

Fund Information (Click: HAPI, HAPY, HAPS)

To learn more, visit harborcapital.com or contact info@harborcapital.com.

About Irrational Capital

Irrational Capital is the investment research firm co-founded by world-renowned behavioral economist Dan Ariely. His goal is to express his behavioral insights via a unique approach to impact investing.

Mr. Ariely specializes in employee motivation and behavioral decision-making.

The firm applies workplace behavioral science, financial acumen, and data science to capture the powerful connection between human capital and financial outcomes.

About Harbor Capital

For over 35 years, Harbor has been serving as a gateway for clients to access talented, institutional caliber asset managers through active, cost-aware investments.

We identify and carefully select specialists in each asset class to manage portfolios, and we apply a comprehensive oversight and monitoring program that keeps the best interests of our clients as the focal point.

By collaborating with expert partners on each targeted strategy, Harbor is not constrained by a single, overarching investment style or viewpoint. This flexibility and diversity of thought allows us to examine any investment approach and enter any asset class, without bias, and has led to a diverse array of investment solutions and insights to meet our clients’ needs.

Important Information

Investors should carefully consider the investment objectives, risks, charges, and expenses of a Harbor fund before investing. To obtain a summary prospectus or prospectus for this and other information, visit harborfunds.com or call 800-422-1050. Read it carefully before investing.

The views expressed herein are those of Harbor Capital and/or Irrational Capital investment professionals at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice.

There is no guarantee that the investment objective of the Fund will be achieved. Stock markets are volatile and equity values can decline significantly in response to adverse issues, political, regulatory, market and economic conditions. The Fund may not exactly track the performance of the Index with perfect accuracy at all times. Tracking errors may occur because of pricing differences, timing and costs incurred by the fund or during times of heightened market volatility.

The Fund relies on the Index provider's methodology in assessing whether a company may be considered a corporate culture leader. There is no guarantee that the construction methodology will accurately assess a company to include or exclude it from the index which could have an adverse effect on the Fund's returns. The Fund's assets may be concentrated in a particular sector or industries to the extent the Index is concentrated and is subject to the risk that economic, political, or other market conditions that have a negative effect on that sector or industry will negatively impact the value of the Fund. The Fund’s performance may be more volatile because it invests primarily in issuers that are smaller companies. Smaller companies may have limited product lines, markets, and financial resources. Securities of smaller companies are usually less stable in price and less liquid than those of larger, more established companies.

There can be no assurance that the Fund will grow to or maintain an economically viable size, in which case the Board of Trustees may determine to liquidate the Fund.

The CIBC Human Capital Index consists of a modified market-weighted portfolio of the equity securities of U.S. companies identified by Irrational Capital LLC (“Irrational Capital”) as those it believes to possess strong corporate culture based on its proprietary scoring methodology. The Index is developed by CIBC World Markets, Inc. (the “Index Provider”), Irrational Capital evaluates companies based on a proprietary, rules-based scoring methodology it developed by leveraging its research in behavioral science, data science and human capital. Constituents of the Solactive GBS United States 500 Index (the “index universe”) at the time of Index reconstitution are eligible for inclusion in the Index. Each company in the index universe that is also identified by Irrational Capital on its list of high-scoring companies (based on the most current scores as of each reconstitution) will be included in the Index. Index constituents in the same sector are weighted based on their float-adjusted market capitalizations. On reconstitution dates, the Index will target the same sector weights as the index universe. If after the Index’s weighting and capping rules are applied, a sector’s weight in the Index would be less than its weight in the index universe, the Index will hold exchange-traded funds that invest specifically in the stocks and securities of the corresponding sector (known as sector ETFs), or such other sector proxy as the Index Provider may determine, to fill the remaining weight and ensure sector neutrality as compared with the index universe. The index listed is unmanaged and does not reflect fees and expenses and is not available for direct investment.

The Human Capital Factor Unconstrained Index is designed to deliver exposure to equity securities of large cap U.S. companies that demonstrate high employee engagement, based on scores produced by Irrational Capital LLC. This unmanaged index does not reflect fees and expenses and is not available for direct investment.

The CIBC Human Capital Factor Small Cap Index is designed to deliver exposure to equity securities of U.S. companies that possess strong human capital, based on proprietary scoring methodology produced by Irrational Capital LLC. This unmanaged index does not reflect fees and expenses and is not available for direct investment.

Alpha is a measure of risk (beta)-adjusted return.

Irrational Capital is a third-party index provider to the Harbor Corporate Culture Leaders ETF.

Foreside Fund Services, LLC is the Distributor of the Harbor ETFs

Citations

- Intangible Asset Market Value Study, 2020

https://oceantomo.com/intangible-asset-market-value-study/ - Diversity, Equity & Inclusion Benchmarking Survey, 2022

https://www.pwc.com/gx/en/services/people-organisation/global-diversity-and-inclusion-survey/global-report-2022.pdf - The 2022 Status Of Remote Work And Top Future Predictions, 2022

https://www.forbes.com/sites/lucianapaulise/2022/12/08/the-2022-status-of-remote-work-and-top-future-predictions/?sh=35f6aa6f1310 - Future of Work Trends 2022, 2022

https://www.kornferry.com/content/dam/kornferry-v2/featured-topics/pdf/FOW_TrendsReport_2022.pdf - Future of Work Reinvented, 2023

https://www.gartner.com/en/insights/future-of-work - Hybrid Work Is Just Work. Are We Doing It Wrong?, 2022

https://www.microsoft.com/en-us/worklab/work-trend-index/hybrid-work-is-just-work - Think Hybrid Work Doesn’t Work? The Data Disagrees, 2022

https://www.gartner.com/en/articles/think-hybrid-work-doesnt-work-the-data-disagrees - The Number of Older Workers Is Growing Quickly as They Continue to Face Economic Challenges, 2022

https://www.jec.senate.gov/public/index.cfm/democrats/issue-briefs?id=0B387CCE-3525-468C-A35F-454A8C49988E - The Over-55 Crowd Is Key to U.S. Workforce Growth. So Is the Over-75 Crowd., 2022

https://www.barrons.com/articles/older-americans-us-workforce-growth-51663360312

2878666