Contact

ContactHarbor Core Bond and Harbor Core Plus Bond: Embracing Complexity To Add Value

August 29, 2023

The U.S. bond market has become increasingly dominated by Treasury bonds. As of June 30, 2023, the Treasury sector made up 41% of the Bloomberg U.S. Aggregate Index, up from 25% in 2008. Consequently, index funds may be challenged to keep up with actively managed strategies, in our view. Index funds have little flexibility and must hold what is in the index, regardless of market conditions. In contrast, active managers can choose to take risk in areas where they think it will be most likely compensated. That’s why often times actively managed strategies underweight Treasuries in favor other market segments such as corporate bonds or mortgage-backed securities.

That said, tilting away from Treasuries alone may not be enough to outperform. Harbor believes that alpha generation in fixed income depends significantly on careful, bottom-up security selection within each sector in the universe.

We were drawn to Income Research and Management (IR+M) to subadvise Harbor Core Bond and Harbor Core Plus Bond because of their experience and expertise in sector allocation and security selection. IRM dedicates an investment staff of 62 with an average tenure of 12 years to researching and uncovering opportunities across the fixed-income universe. The team supports and manages several strategies that span most sectors of the bond market, giving them a broad view across the opportunity set.

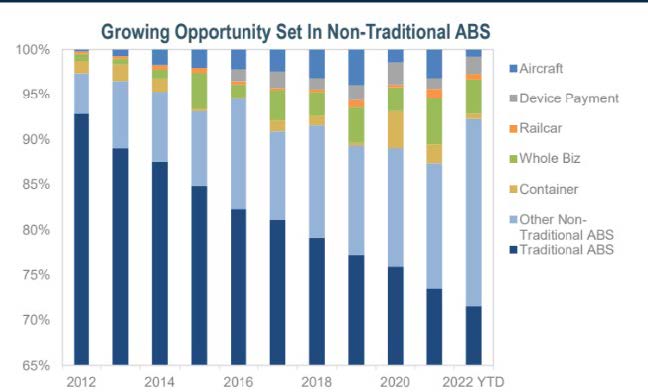

Furthermore, the firm’s experience and resources help give them the ability to look in areas where others may not. For example, IR+M has long favored non-traditional asset-backed securities as a way to add value over the benchmark. The non-traditional ABS market is a growing market segment (see chart). Yet because of index-inclusion rules, many of these securities are not index eligible and are therefore off the radar screen of passively oriented bond investors.

Source: JP Morgan as of 6/30/22. Chart shows ABS issuance “Other nontraditional ABS” includes unsecured consumer, miscellaneous, solar, time share, insurance, taxes, SBL, trade receivable, healthcare, royalties, stranded asset, and infrastructure, while “Traditional ABS” includes credit cards, auto, student loans, equipment, global RMBS, and floorplan.

The ABS market is diverse and spans a wide variety of collateral types, such as airline and railcar leases, storage containers, music royalties, and franchise fees, among others. Furthermore, some ABS have complex structures that can take time to understand. As a result, these bonds can be mispriced, providing opportunities for those investors with the bandwidth and expertise necessary to evaluate them.

IR+M has spent decades following the ABS market and has the resources necessary to research these securities to make thoughtful security selection decisions, in our view. Indeed, IR+M views analysis of ABS to be a core competency and a distinguishing feature of their approach and their portfolios. This has the potential to help in two ways: 1) in separating the wheat from the chaff in this space--zeroing in on those ABS issues believed to be offering the most attractive risk-adjusted return opportunities and 2) in having expertise across subsectors— in an effort to build a diversified exposure. As of June 30, 2023, Harbor Core Bond and Harbor Core Plus Bond allocated 8.2% and 10.0%, respectively to ABS, compared to just 0.5% for the fund’s benchmark – the Bloomberg U.S. Aggregate Index.

IR+M’s ABS expertise complements the firm’s other core competency – detailed analysis of corporate bonds – carried out by a dedicated team of credit specialists. The team conducts robust and thorough research, favoring bonds issued by financially solid companies with durable business models.

In addition to its security selection expertise, IR+M also aims to add value via skillful sector allocation, which is informed by the firm’s broad view of the fixed income market. The firm’s seven person investment committee continuously and dynamically allocates portfolios across various fixed income sectors based on sector-relative valuations, liquidity conditions and risk measures. The team likes to say that they “take what the market gives them,” which allows them to be nimble and flexible without making macro-oriented decisions (which they believe is extremely difficult to time and get right consistently) based on duration or the shape of the yield curve.

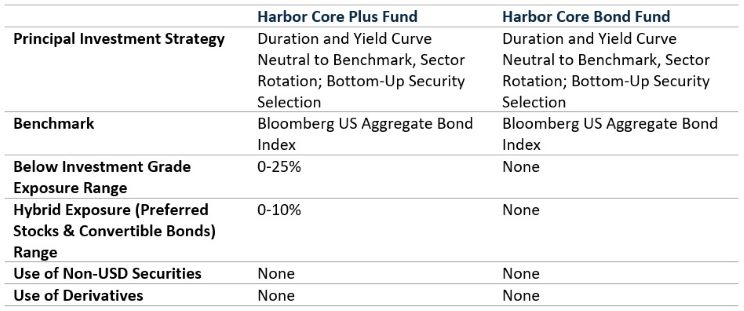

Combined, we believe these capabilities are a powerful source of potential added value that gives IR+M an edge over their peers in the core and core plus universe. Harbor offers investors two ways to benefit from IR+M’s expertise.

Important Information

The views expressed herein may not be reflective of current opinions, are subject to change without prior notice, and should not be considered investment advice or a recommendation to purchase or sell a particular security.

There is no guarantee that the investment objective of the Fund will be achieved. Fixed income investments are affected by interest rate changes and the creditworthiness of the issues held by the Fund. As interest rates rise, the values of fixed income securities held by the Fund are likely to decrease and reduce the value of the Fund's portfolio. There may be a greater risk that the Fund could lose money due to prepayment, extension risks, value fluctuation in response to market perception of issuer creditworthiness, because the Fund invests, at times, in mortgage-related and/or asset backed securities. The market for convertible securities is less liquid than the market for non-convertible corporate bonds.

The Bloomberg U.S. Aggregate Bond Index is an unmanaged index of investment-grade fixed-rate debt issues with maturities of at least one year. This unmanaged index does not reflect fees and expenses and is not available for direct investment.

Alpha is a measure of risk (beta)-adjusted return.

Duration is a commonly used measure of the sensitivity of the price of a debt security, or the aggregate market value of a portfolio of debt securities, to change in interest rates. Securities with a longer duration are more sensitive to changes in interest rates and generally have more volatile prices than securities of comparable quality with a shorter duration.

A yield curve is a line that plots yields, or interest rates, of bonds that have equal credit quality but differing maturity dates.

Diversification does not assure a profit or protect against loss in a declining market.

3085877