Contact

ContactFixed Income: Complexity Favors Active Strategies

August 29, 2023

Client expectations about passive strategies in fixed income may be framed by what they see in the equity market. However, the bond market is larger and more complex, which can pose challenges for passive strategies. The U.S. fixed income measures approximately $55 trillion in size and encompasses a wide variety of debt types, such as investment grade and high yield corporate bonds, federal agency debentures, and mortgage backed securities. Compare that to the U.S. equity market, which measures approximately $46 trillion and is composed almost entirely of just one security type – the common equity of publicly traded corporations. The complexity of the fixed income universe is perhaps even better illustrated from the bottom up: Apple has one common stock that trades under the ticker AAPL; however, Apple has dozens of bonds outstanding, each with different structures and terms.

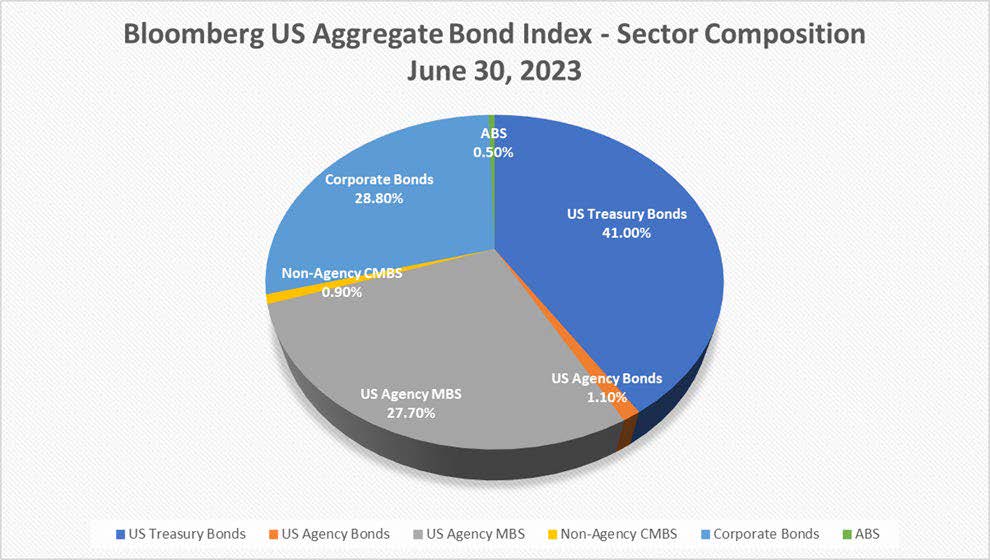

As a result, it is not a straightforward task to construct a benchmark that represents the broad fixed-income universe. Consequently, ETFs that track broad bond benchmarks face structural challenges. For instance, bond indexes are generally constructed to place more weight on issuers who borrow the most. For the investment grade universe that means the U.S. government. Because of the significant increase in government borrowing over the past several years, Treasury bonds represent a significant chunk of the bond market. Treasury securities represented 41% of the Bloomberg U.S. Aggregate Bond Index as of June 30, 2023, up from 25% in 2008.

Source: Bloomberg

Granted, Treasury bonds are supported by the full faith and credit of the U.S. government, meaning credit risk is lower compared to other fixed-income market segments. Consequently, investors accept lower return prospects compared to comparable maturity bonds in other sectors. However, as investors have recently been made painfully aware, Treasuries and government securities are not completely risk free and can be vulnerable to rising interest rates. To illustrate, the Bloomberg U.S. Government Index declined 12.3% in 2022 as interest rates rose from record low levels.

Because of the Bloomberg U.S. Aggregate Index’s construction methodology, passive core strategies that track the index are dominated by Treasury bonds. In contrast, active core and core plus managers have more flexibility to improve diversification and emphasize sectors that may offer better risk-reward profiles than Treasuries. In fact, often actively managed strategies favor corporate bonds over Treasuries.

However, tilting away from Treasuries alone may not be enough to outperform the competition. We believe that consistent alpha generation in fixed income depends significantly on careful, bottom-up security selection within each sector in the universe. That’s why we think investors should favor active strategies managed by experienced portfolio managers with the skill and resources necessary to conduct robust credit research across the fixed income universe.

Important Information

The views expressed herein may not be reflective of current opinions, are subject to change without prior notice, and should not be considered investment advice or a recommendation to purchase or sell a particular security.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses. Fixed income investments are affected by interest rate changes and the creditworthiness of the issues.

The Bloomberg U.S. Aggregate Bond Index is an unmanaged index of investment-grade fixed-rate debt issues with maturities of at least one year. The Bloomberg U.S. Government Index comprised of the U.S. Treasury and U.S. Agency Indices. The index includes U.S. dollar denominated, fixed-rate, nominal U.S. Treasuries and U.S. agency debentures (securities issued by U.S. government owned or government sponsored entities, and debt explicitly guaranteed by the U.S. government). These unmanaged indices do not reflect fees and expenses and are not available for direct investment.

Alpha is a measure of risk (beta)-adjusted return.

Diversification does not assure a profit or protect against loss in a declining market.

3085817