Contact

ContactDo Interest Rate Bets Pay Off?

March 15, 2024

Core and core plus managers have several arrows in their quiver. For instance, they can seek to add value through careful security selection, sorting through the bond universe for issuers with strong fundamentals such as healthy balance sheets and ample cash flow. Sector rotation – where the manager tilts the portfolio toward more encouraging areas of the market – is another tool for potentially adding value. Most funds in the core and core plus universe make use of these tactics.

In addition, some managers also seek to add value by positioning their funds’ durations based on their outlook for interest rates. These macro calls can be challenging because interest rates can be notoriously difficult to predict with consistency — even for experts. Furthermore, interest rate bets can be problematic from a risk-control perspective because they can be difficult to diversify, leaving funds vulnerable when the managers get their rate calls wrong. This is in stark contrast to bottom-up security selection where a fund manager can diversify across hundreds of securities and issuers. Because of these challenges, some core and core plus managers take the view that interest rate forecasting is a low probability tactic, and they consequently avoid them. Nevertheless, there are some high profile firms that spend significant time and resources on developing interest rate views that guide the positioning of some of the largest core and core plus strategies in the market.

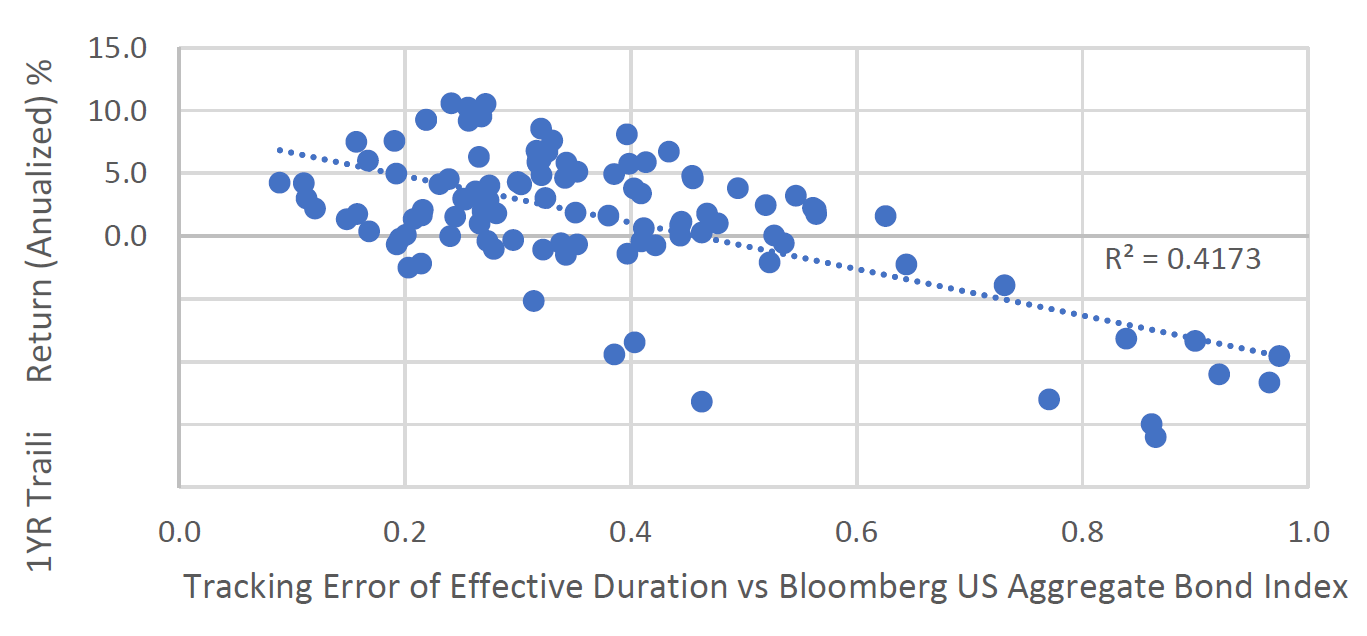

To dig a bit deeper on this topic, we recently conducted a study to gauge the success of core plus funds that include interest rate bets as part of their process*. We defined an interest rate bet as the difference between a fund’s duration and the duration of the Bloomberg US Aggregate Bond Index (the US Agg). We then measured the frequency and magnitude of interest rate bets by calculating the tracking error of those differences. Funds with high tracking errors are those that varied their durations significantly and frequently, meaning they made meaningful use of interest rate bets in their process. If interest rate calls were effective, we would expect to see a positive relationship between tracking error and returns. If they were not, we would expect to see a negative relationship.

Trailing 12-Month (rolling monthly, annualized)

Jan 2015 - Jan 2024

Source: Morningstar Direct. All returns are total and net of fees.

The scatter plot above depicts the tracking error of duration bets versus the average annual rolling 1-year returns. It clearly shows a negative relationship between funds with large swings in duration versus the US Agg and rolling 1-year returns. Said another way, funds that varied their durations the least tended to perform better. This leads us to suspect that interest rate bets are a low percentage tactic and suggests that investors may be better off favoring funds that avoid making big calls on rates.

A Potential Solution

For an attractive option that opts to forego taking on interest rate risk relative to its benchmark, we point to the Harbor Core Plus Fund. The Fund leans on the robust experience of its investment team, utilizing a straightforward durationneutral, bottom-up approach that focuses on selecting attractive cash bonds from creditworthy issuers in pursuit of steady returns. To learn more, please visit our website.

Important Information

For institutional investors only.

The views expressed herein are those of Harbor Capital Advisors, Inc. investment professionals. They may not be reflective of current opinions, are subject to change without prior notice, and should not be considered investment advice.

Investing involves risk, including the possible loss of principal.

There is no guarantee that the investment objective of the Fund will be achieved. Fixed income investments are affected by interest rate changes and the creditworthiness of the issues held by the Fund. As interest rates rise, the values of fixed income securities held by the Fund are likely to decrease and reduce the value of the Fund's portfolio. There may be a greater risk that the Fund could lose money due to prepayment and extension risks because the Fund invests, at times, in mortgage-related and/or asset backed securities.

The Bloomberg US Aggregate Bond Index is an unmanaged index of investment-grade fixed-rate debt issues with maturities of at least one year. This unmanaged index does not reflect fees and expenses and is not available for direct investment.

*Requirements for inclusion in this analysis included all U.S. open-end and ETF Funds in the US Intermediate CorePlus Morningstar category.

Source of all data and calculations are produced by Morningstar Direct unless other source noted. © 2024 Morningstar, Inc. All rights reserved. The information contained herein: (1) is proprietary to Morningstar and/or its content providers; (2) may not be copied or distributed; and (3) is not warranted to be accurate, complete, or timely. Neither Morningstar nor its content providers are responsible for any damages or losses arising from any use of this information. Past performance is no guarantee of future results.

Calculation information: Median return is trailing 1YR returns, rolling monthly and annualized (1/31/20151/31/2024). Tracking Error of Effective Duration is the rolling 12M STD, annualized, of the monthly difference between the category’s median effective duration and the effective duration of the Bloomberg U.S. Aggregate Bond Index from FactSet.

Investors should carefully consider the investment objectives, risks, charges and expenses of a Harbor fund before investing. To obtain a summary prospectus or prospectus for this and other information, visit harborfunds.com or call 800-422-1050. Read it carefully before investing.

Income Research + Management is an independent subadvisor to the Harbor Core Plus Fund.

Harbor Funds Distributors, Inc. is the Distributor of the Harbor Mutual Funds.

3446673