Contact

ContactMay CPI: Moving on Down

June 14, 2023

Executive Summary:

- Steady disinflation continued with the May Consumer Price Index (CPI) print reinforcing expectations that the Federal Open Market Committee (FOMC) will skip a rate hike at the June meeting.

- The Committee intends to signal a July resumption for hikes, but Chair Powell’s guidance and history suggest that the hiking cycle may have ended in May.

- Budding enthusiasm for a soft landing should be tempered as it means higher rates for longer, which poses a threat to valuations.

- Risk/reward continues to favor being cautious here as lofty valuations require a quick pivot to interest rate cuts and resilient growth, two things we do not expect.

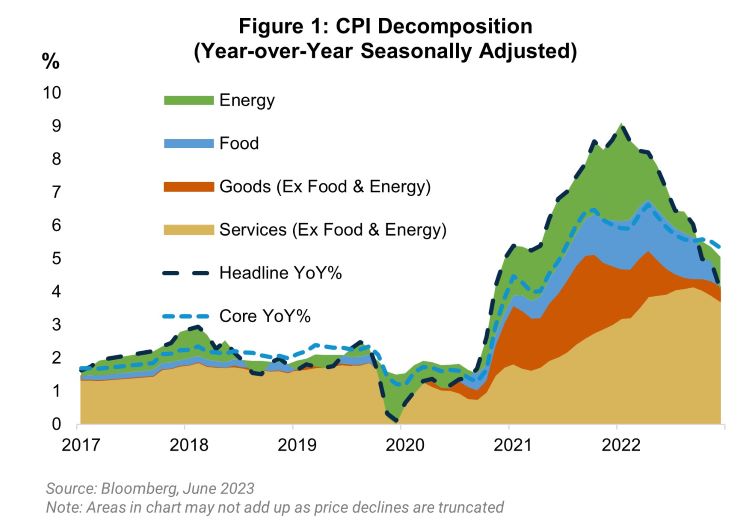

Headline and core CPI for May came in at 4.1 and 5.3 percent year-over-year, respectively, giving the FOMC the greenlight to leave rates unchanged at their June meeting. At the headline level, price growth was subdued as energy price declines subtracted 25 basis points1 from the month-over-month figure. For core, the 0.4 percent increase resulted from a jump in used car prices and shelter costs remaining elevated relative to pre-COVID trends. However, trends in wholesale car prices and private market rents give the FOMC confidence that price growth in both sectors is heading lower. Most importantly, core services, excluding shelter, are closer to the FOMC’s 2 percent target.

A Skip or A Pause

Chair Powell and several other prominent members of the Committee pre-signaled over the intermeeting period that the FOMC planned to keep rates on hold at their June meeting. The decision to keep rates on hold was framed as a way for the Committee to see further evidence about the effects of policy tightening on the real economy before hiking further. The decision was whether to skip a meeting versus hike rather than mark an end to the hiking cycle entirely. The best case for a pause was that more time assures the Committee that the financial stability concerns relating to the bank failures were subsiding. This reasoning never made much sense as the data received since the May meeting continued to show a resilient economy and firm wage growth, while an additional month of banking data could not answer the franchise value questions bedeviling smaller banks.

The tortured logic behind the skip makes for a difficult press conference for Chair Powell. We expect the Committee’s Summary of Economic Projections (SEP) to indicate one additional hike in 2023 with Chair Powell communicating that the July meeting is the default for that hike. Skipping a hike at the June meeting was clearly the Chair’s preference while many other FOMC participants, possibly even a majority, preferred a hike in June. To placate their policy leanings in exchange for a skip, Powell is likely to firmly argue that rates are moving higher and staying there for the duration of the year. We will be focused on what the SEP dots show for 2024 and 2025 as the market continues to price in a lower rate path, which we think reflects the market’s weighting of recessionary outcomes rather than a huge gap in the most likely outcome for the FOMC and the market.

While we expect Powell to endorse the skip, we think his early messaging on the June meeting indicates that he thinks the hiking cycle is at its end. The historical record suggests that once the Committee pauses rate hikes, more often than not, they do not restart. A one meeting skip is not unprecedented, but we think the strategy behind his thinking after the May meeting was that skipping the June meeting allowed for further evidence to pile up in favor of an end to the hiking cycle rather than clearing the way to continue following the banking bank failures. A hike in July is the baseline and will be the message as it reflects most of the Committee; however, do not be surprised if additional evidence in June and July supports Chair Powell’s revealed preference.

A Soft Landing For The Economy But Not The Equity Market?

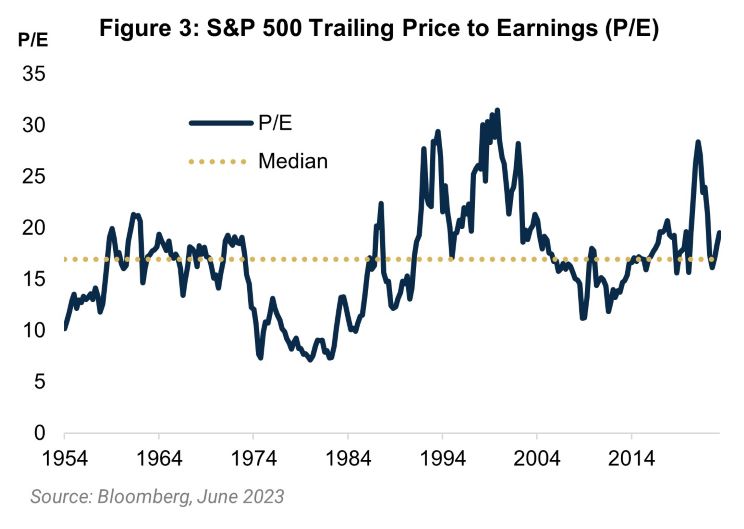

Amid the enthusiasm around artificial intelligence, multiple expansion largely explains the strong equity market performance year-to-date rather than material upward revisions to earnings estimates. While we are still pessimistic about the U.S. economy in the near-term, the question we are trying to answer is what the right multiple is should the Fed engineer disinflation without a further deceleration in growth. At 20 times trailing earnings, the U.S. market is almost one standard deviation2 above its 70-year average and looks more elevated on a cyclically adjusted basis. Some secular expansion in the multiple makes sense as margins expanded; however, we think much of this owes to an embedded assumption that interest rates will decline soon after the end of the Fed’s hiking cycle.

A soft landing from here directly challenges that assumption. So far, rate hikes have slowed the housing market, growth is running below the Fed’s estimate of potential, meanwhile the labor market continues to be robust. If 6 months from now, the unemployment rate is around 4 percent, inflation is consistent with 2 percent, and growth has not decelerated further, rate cuts are not happening. The assumption behind cuts is that the high rates of today exceed the neutral rate, an unobserved variable, and will continue to suppress the economy. However, the best evidence for the neutral rate is how the labor market is responding to interest rates. An unemployment rate of 4 percent with stable growth and inflation runs counter to the FOMC’s estimate of a 2.5 percent nominal neutral rate. The result is a steeper curve and higher long-term interest rates in this scenario.

We think a 20x multiple is a hefty valuation for a world offering 5 percent yields on Treasuries. Putting together our scenarios, upside from here requires a soft landing with falling interest rates in 2024 and 2025 or an acceleration in productivity that leads to earnings revisions. We are skeptical on both fronts. And all of this is before accounting for the high risk of a recession this year or next. We remain underweight risk assets, focused on quality across our fixed income and equity portfolios, and neutral duration to account for the risks posed by a soft landing.

For more information, please access our website at www.harborcapital.com or contact us at 1-866-313-5549.

Important Information

1 A basis point is one hundredth of 1 percentage point.

2 Standard deviation measures the dispersion of a dataset relative to its mean.

The views expressed herein are those of Harbor Capital Advisors, Inc. investment professionals at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice. The information provided in this presentation is for informational purposes only.

This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy.

Performance data shown represents past performance and is no guarantee of future results.

The price-to-earnings (P/E) ratio is the ratio for valuing a company that measures its current share price relative to its earnings per share (EPS).

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

2955326