Contact

Contact

FOMC Makes 50 Basis Points Look Easy

June 07, 2022

Executive Summary:

- Chair Powell and the Federal Open Market Committee (FOMC) delivered no surprises at the May FOMC meeting, which prompted a relief rally in bonds and equities.

- The knee-jerk reaction in markets stemmed from Powell’s comment that the Committee is not actively considering a 75 basis point hike. The probability of that was always low and today’s statement and press conference provided limited new information.

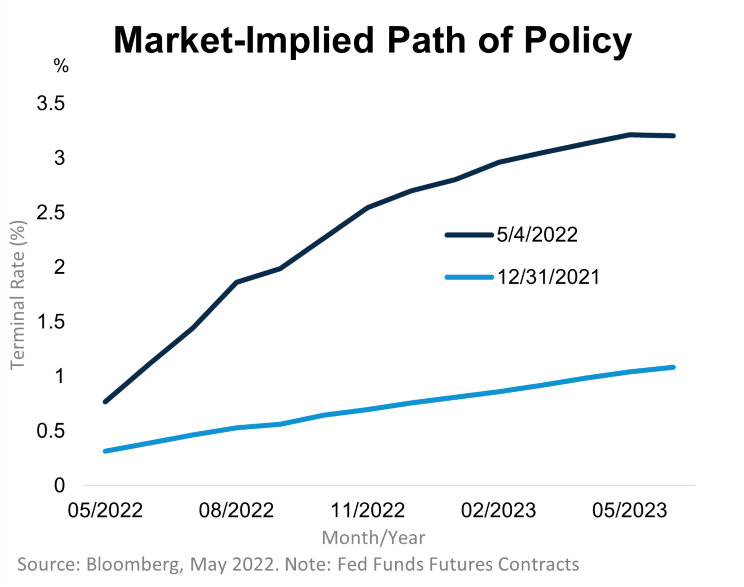

- The Committee appears content to follow the market-implied path of policy as they await further clarity on the trajectory for inflation. Another 50 basis point hike at both the June and July meetings is now our baseline assumption.

- Our positioning remains the same. Stay close to benchmark allocations in equities and fixed income, while tilting towards more defensive and higher quality exposures within each asset class.

FOMC Delivers Just What the Market Ordered

Despite late speculation that the FOMC might surprise markets with a 75 basis point1 hike after Federal Reserve (Fed) President Bullard’s trial balloon immediately prior to the communications blackout, the Committee increased rates by 50 basis point and announced that balance sheet reduction would start on June 1st. On the latter, the Committee announced that Treasury and Agency mortgage-backed securities (MBS) would decline by $30 and $17.5 billion per month, respectively, from June through August after which the pace will double.2 Both decisions were aligned with market expectations and were well-telegraphed by the FOMC over the intermeeting period.

During the press conference, Powell indicated that additional 50 basis point hikes were “on the table at subsequent meetings;” i.e., they are the most likely outcome for June and July at a minimum. However, he successfully demurred on the likelihood of 75 basis point hikes by reiterating that the Committee plans to increase interest rates expeditiously this year. There is not a strong economic case to do a string of 50 basis point hikes rather than frontloading tightening via 75 basis points hikes. Rather the decision in favor of 50 reflects the Committee’s wariness to surprise markets when market pricing already reflects a substantial further tightening in financial conditions. A policy surprise is reserved for a time when markets are ignoring the FOMC’s intentions.

Finally, as to balance sheet reduction, aka quantitative tightening, the Committee’s plans are now clear, and the only uncertainty is the pace of Agency MBS prepayments in the months to come. Given the increase in mortgage rates and early signs that affordability is becoming a concern for potential home buyers, it is unlikely that Agency MBS maturities will reach the $35 billion cap. The combination of slower Agency MBS prepayments and the Treasury Department’s improved fiscal outlook after the April tax date should modestly reduce upward pressure on interest rates from balance sheet reduction. As Powell noted, the effects of balance sheet reduction are uncertain and we do not expect it to be a prominent contributor to tighter financial conditions until reinvestment caps are fully phased in and well underway.

Abandoning Forward Guidance for Now

The biggest takeaway from today’s meeting, besides brushing aside 75 basis point hikes, is that Chair Powell and the Committee are comfortable with market pricing for the hiking cycle and recognize the limited utility of forward guidance in the current environment. At face value, markets are pricing roughly 9 more hikes through the middle of 2023 with a terminal rate between 3-3.5 percent. However, as Powell intimated repeatedly in the press conference, comfort in market pricing does not imply confidence in their neutral rate estimates nor the right level of financial conditions to achieve a soft landing. Uncertainty abounds with the war in Ukraine, lockdowns in China, and whatever exogenous shock may follow. Absent a significant easing or tightening of financial conditions, the Committee appears happy to deliver on market pricing in the near-term until the inflation outlook becomes clearer.

Too Late for Risk, Too Soon for Safety

Admittedly, the magnitude of today’s rally was surprising and our confidence in where prices go in the near-term is low. But the medium-term direction for asset prices remains the same. Financial conditions are tighter today and the real economy will reflect that through slowing growth in the months to come. Moreover, the risk that high inflation persists remains elevated whether that risk stems from exogenous shocks or because the U.S. economy is overheating. In this environment, we favor a neutral stance in equities with a tilt towards more defensive and higher-quality exposures like healthcare. For fixed income, we tilt in the same direction and prefer higher-rated exposures in Treasuries, Agency MBS, and, to a lesser degree, investment grade credit. However, it is too soon to become outright defensive via a duration overweight and equity underweight. We believe we are closer to the end of the cycle than the beginning, but business cycles don’t die of old age, and we think the likelihood of a recession in 2022 remains low.

For more information, please access our website at www.harborcapital.com or contact us at 1-866-313-5549.

Legal Notices & Disclosures

1 Basis points refers to a common unit of measure for interest rates and other percentages in finance. One basis point is equal to 1/100th of 1%, or 0.01%, or 0.0001, and is used to denote the percentage change in a financial instrument.

2 The Desk implements balance sheet reduction through monthly maturity caps; i.e., the Committee sets the maximum amount of balance sheet reduction that can occur in a given month. For Agency MBS, the monthly decline in holdings depends solely on Agency MBS proceeds, which fluctuates based on mortgage prepayment rates. For Treasuries, the monthly decline depends on the maturity schedule of the SOMA Treasury holdings and will reach the cap for the foreseeable future until they exhaust the supply of Treasury bills in 2023.

The views expressed herein are those of Harbor Capital Advisors, Inc. investment professionals at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice. The information provided in this presentation is for informational purposes only.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

Harbor Capital Advisors, Inc.

2229041