Contact

ContactBeyond Inflation, The Tailwinds for Commodities May Persist for Years

November 11, 2022

Key Takeaways:

- The high liquidity, low interest rate environment that fueled the high growth stock boom for the past decade known best as the “T.I.N.A.” trade which stands for “There is no alternative” has run into a brick wall courtesy of the Federal Reserve’s (Fed) battle against inflation.

- Inflation has been stoked by geopolitical disruptions, driving interest rates higher and consequently stocks and bonds lower as economic growth concerns mount, leaving investors in search of asset classes which are built to weather this new regime.

- Commodities have historically delivered significant benefits during periods of rising inflation and beyond.

- The time for allocation to real assets, or “T.A.R.A” has arrived and likely only in the early innings with room to run.

Introduction

Since the Great Financial Crisis of 2008, the Federal Reserve has provided highly accommodative monetary policy which created an environment of cheap money, and historically low market volatility. The dovish stance positioned the Federal Reserve as a friend of the market, ready to act as the “Fed Put” when the economy and markets showed any sign of wavering stability and strength. This was an environment that gave birth to the investing philosophy that, “There Is No Alternative” to equities, or the “T.I.N.A.” trade. This ultimately drove investors to underweight their holdings in diversifying asset classes like fixed income and commodities with the belief that inflationary pressures were indefinitely suppressed, and risk assets were the only game in town.

The T.I.N.A. trade became further supercharged when ultra-accommodative monetary policy ensuing the COVID-19 global pandemic, once again taking real interest rates into negative territory, and pulling forward earnings of T.I.N.A. beneficiaries across high growth sectors like Information Technology. However, the shock also caused a massive supply chain disruption which set the stage for commodities to demonstrate their importance as portfolio diversifiers and inflationary hedges.

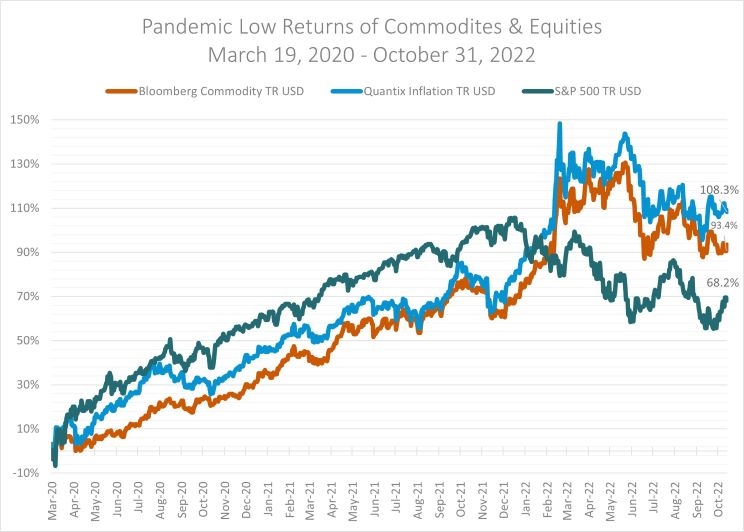

Commodities have enjoyed a return to the limelight since the pandemic lows set back in March 2020, when crude oil futures traded in negative territory as the world came to a standstill, crushing demand for virtually every commodity sector. Since then, the Bloomberg Commodity and Quantix Inflation Indexes have returned 93.4% and 108.3% through the end of October 2022 respectively, besting the S&P 500 by 25.2% and 40.1% as supply and demand imbalances fueled a strong rebound in demand.

Figure 1

Source: Morningstar Direct, October 2022

The Federal Reserve, from Friend to Foe… Is it Too Late to Invest in Commodities?

In the aftermath of stimulus, inflation has reached multi-decade highs and become the focal point of concern for investors. Subsequently, commodities have provided a robust inflationary hedge, however the specter of recession and demand destruction driven by high interest rates, a strong US Dollar and stratospheric commodities prices have prompted investors to question if this “trade” is over. We believe the answer is no, and this resurgence is only in the early innings.

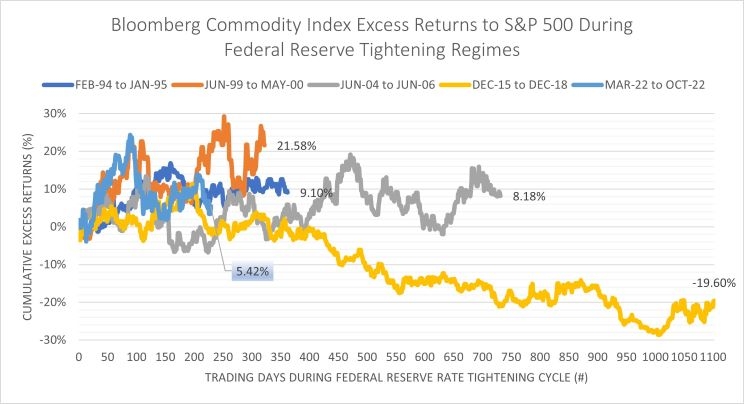

Looking at historical rate tightening regimes, commodities as measured by the Bloomberg Commodity Index have generated positive excess returns relative to the S&P 500 in 4-of-5 rate hike cycles going back to 1994. These periods can be volatile as markets try to gage the impacts of higher interest rates and have regularly experienced maximum drawdowns averaging more than 10% before the end of the rate tightening cycle as illustrated in Figure 2.

Figure 2

Source: Morningstar Direct, October 2022

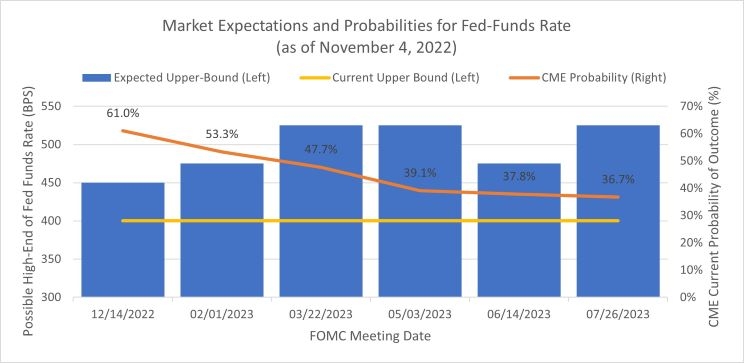

Additionally, rate hikes are expected to continue throughout 2022 and into 2023 in order to tame inflation, further supporting the argument for commodities as a portfolio hedge to additional inflation pressures.

Figure 3

Source: FactSet Policy Rate Tracker, October 2022

Commodities Futures Markets have a Structural Tailwind

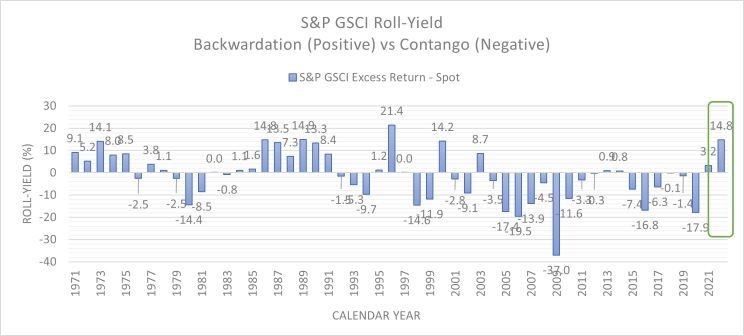

While conventional wisdom suggests that rising interest rates present headwinds for most commodities, other forces such as supply and demand imbalances can be an even more influential driver of returns. This situation results in a change in the shape of the futures curve that rewards commodity investors in the form of a positive roll-yield for simply buying a commodities contract and then rolling into a less expensive contract ahead of expiration. Energy and base metals sectors which make up the largest weights in most commodity indexes are in a state of backwardation.

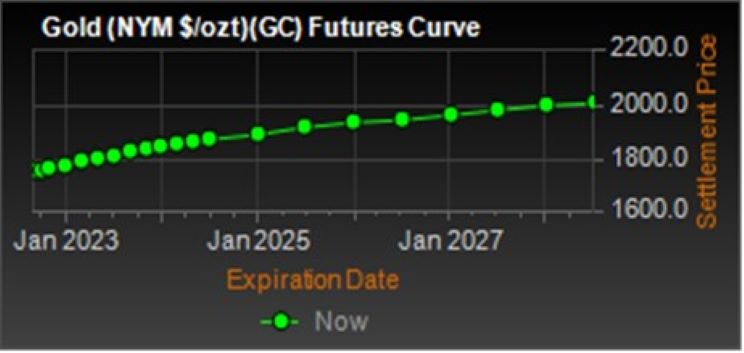

Backwardation and contango are quickly moving from esoteric terms into the mainstream. Without getting too nerdy, contango and backwardation are terms used to define the structure of the forward curve. When a market is in contango, the forward price of a futures contract is higher than the spot price. Conversely, when a market is in backwardation, the forward price of the futures contract is lower than the spot price. In the charts below, you can see that Crude Oil WTI is currently in backwardation as contracts further out are priced lower than the current spot price, while Gold contracts are in contango.

Figure 4

Source: FactSet, October 2022

The primary reason a backwardation pricing situation happens is a shortage of the underlying asset in the spot market, causing market participants to pay a premium to buy the immediately deliverable commodity. Since futures prices tend to rise over time and converge with the higher spot prices, backwardation favors those traders and investors who are net long, and these regimes have historically lasted for several years at a time when they are present.

Figure 5

Source: Morningstar Direct, October 2022

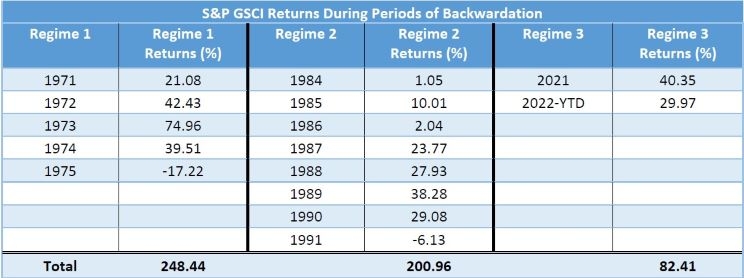

While commodities can be volatile, history has shown that in both backwardation and contango, the regimes have tended to persist for many years at a time and have marked periods of rewarding returns for investors. Figure 6 shows cumulative returns of 248% and 201% as measured by the S&P GSCI from 1971-1975 and 1984-1991. The current period beginning January 2021 – October 2022 have already realized returns of 82.4%.

Figure 6

Source: Morningstar Direct, October 2022

Given the current structural challenges with supply chain disruptions and shortages, these imbalances may persist for many years indicating that we’re in the early innings of this cycle with a long runway ahead.

However, once inflation begins to subside and the structural tailwinds of supply shortages begin to ease, will the benefits of commodities also fade away?

Beyond Inflation, Commodities Enhance Diversification

Diversification is often the best tool that investors have for navigating through periods of volatility. However, since the Federal Reserve meeting in November 2021, stocks and bonds have been experiencing rising levels of correlation which has resulted in the tried-and-true 60/40 portfolio experiencing its worst start to a year in its history. This has caused investors to reconsider what investments a well-diversified portfolio should contain.

Over this time period, commodities have demonstrated consistently low levels of correlation to both stocks and bonds, providing important diversification benefits to investor portfolios.

Figure 7

Source: Morningstar Direct, October 2022

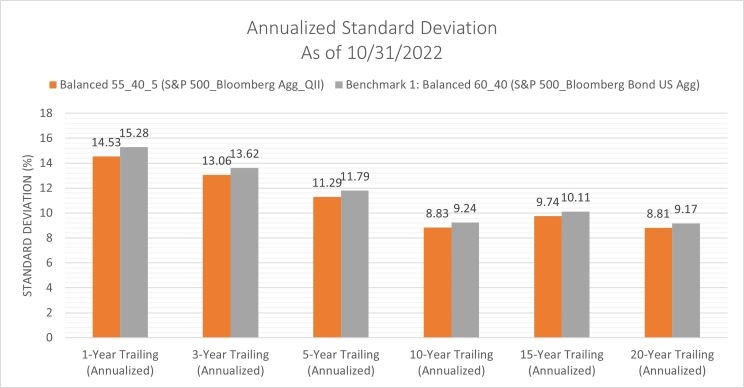

Lastly, some investors have shunned commodities because they are viewed as a particularly volatile asset class. However, given that commodity prices are mainly driven by the balance of supply and demand, they have generally been less sensitive to stock and bond market returns over time. The hypothetical portfolios shown in Figure 8 highlight how even a small allocation to “riskier” commodities can reduce overall levels of volatility compared to a traditional 60/40 portfolio.

Figure 8

Source: Morningstar Direct, October 2022

The data and information noted above is based on hypothetical assumptions. It is for informational and illustrative purposes only. This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy. The hypothetical estimates presented do not represent the results that any particular investor may actually attain. Actual performance results will differ, and may differ substantially, from the hypothetical estimated performance.

Conclusion

Commodities have experienced a renaissance over the course of the past couple of years, which has caught many investors off guard. While no one knows precisely when inflation will peak or commodity supply and demand imbalances will correct, we do know that these regimes tend to last for years and the benefits of having commodities as a part of a diverse portfolio are evident. So instead of looking to market time a trade, look to having a strategic allocation to commodities which can deliver benefits well beyond the ones being enjoyed in today’s market environment, as the Time to Allocate to Real Assets (T.A.R.A.) is now.

For more information, please access our website at www.harborcapital.com or contact us at 1-866-313-5549.

Important Information

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

The views expressed herein are those of Harbor Capital Advisors, Inc. investment professionals. They may not be reflective of current opinions, are subject to change without prior notice, and should not be considered investment advice.

Diversification does not assure a profit or protect against loss in a declining market.

The Bloomberg Commodity Index (BCOM) is a broadly diversified commodity price index distributed by Bloomberg Index Services Limited. It is calculated on an excess return basis and reflects commodity futures price movements. The index rebalances annually weighted 2/3 by trading volume and 1/3 by world production and weight-caps are applied at the commodity, sector, and group level for diversification. Roll period typically occurs from 6th-10th business day based on the roll schedule.

The Bloomberg US Aggregate Bond Index is an unmanaged index of investment-grade fixed-rate debt issues with maturities of at least one year. This unmanaged index does not reflect fees and expenses and is not available for direct investment.

The Quantix Inflation Index is calculated on a total return basis, which combines the returns of the futures contracts with the returns on cash collateral invested in 13-week U.S. Treasury Bills. This unmanaged index does not reflect fees and expenses and is not available for direct investment. The Quantix Inflation Index was developed by Quantix Commodities LP and is owned by Quantix Commodities Indices LLC.

The S&P 500 Index is an unmanaged index generally representative of the U.S. market for large capitalization equities. This unmanaged index does not reflect fees and expenses and is not available for direct investment.

The S&P GSCI is a composite index of commodities that measures the performance of the commodities market. The index often serves as a benchmark for commodities investments.

2590307