Contact

ContactAI to The Rescue

August 23, 2023

Given the impact of artificial intelligence (AI) on global markets in the first half of 2023, subadvisor C WorldWide dove deeper into the implications of the AI disruption for investors. They astutely note that “there are good reasons for excitement, but a grain of realism is needed not expecting AI to solve all world problems.” What is more certain is C WorldWide’s thoughtfulness on this topic, as evidenced by their below reflections.

AI to The Rescue

On the surface, it appears that investors worldwide have ignored the recession risk given the positive equity market return of 14% in the first half of 2023 as measured by the MSCI AC World Index in USD. But if we scratch the surface, the old U.S. Dow Jones Industrial Index rose only 4%, while the technology-heavy Nasdaq Composite rose an impressive 32%.

This extreme divergence is driven by the launch of ChatGPT in late 2022. This defining point in time, compared by many to the launch of the iPhone in 2007, has fueled speculation and hopes for renewed growth in a technology sector that experienced a peak during Covid. Investors have rewarded technology giants such as Apple, Microsoft, Nvidia, Google, Amazon and Facebook, as well as Tesla, which have all risen more than 35%. This pronounced concentration is illustrated by the fact that 10 stocks in the S&P 500 accounted for 90% of the market return in 2023 (source: Bernstein Research, calculated as of 12 June 2023).

“The healing journey for the stock market continues with a potential peak and pause in interest rate hikes. Optimism seems to dominate for now, given the exciting promises of AI.”

We believe the market is in a healing process after the wounds inflicted by the escalating inflation post the Covid period and the ensuing powerful and historical response of the central banks. The equity market fall in 2022 brought the overall valuation metrics sharply lower as overall corporate earnings continued to rise. Our assessment over the past quarters has been that the stock market is moving ahead in the healing journey as the end of interest rate hikes appears to be nearing.

Optimism also seems to dominate for now as the exciting promise of AI has driven up equity prices. AI can produce large productivity gains across multiple industries with the potential to automate 300 million administration jobs, as estimated by Goldman Sachs. The dominant technology companies are in an attractive position, as they have access to valuable data and, at the same time, possess the enormous resources needed to bring the best AI solutions to the market. These solutions can be sold as an integral part of the existing and established products already familiar to companies and consumers. However, we also see good opportunities for traditional industrial companies to combine artificial intelligence with vision sensors and tools, further improving productivity in the more tangible world. The possibilities also extend into a more intelligent next-generation energy infrastructure.

As with any technological breakthrough, there is an excitement phase, and that’s where we are currently. There are good reasons for excitement, but a grain of realism is needed not expecting AI to solve all world problems. We are following the AI revolution which will probably be more of an evolutionary process, and we have a particular focus on understanding specifically how companies bring out new innovative products and services.

A Concentrated Market Isn’t a Danger Signal Per Se

A rising stock market driven by few companies could question the sustainability of the upward trend. For instance, during the IT bubble around the year 2000, the market fell sharply after the explosive IT-driven bull market and didn’t recover for many years afterwards.

However, a recent analysis from Bernstein Research shows that a concentrated market advance is not necessarily a danger signal. In the late 90s and early 2000s, the valuation of the dominant IT companies increased dramatically, but this is not the case this time. The valuation of the leading companies (the 10 companies that have driven most of the market gain this year) has increased from a p/e of 21x at the beginning of the year to 32x, with Microsoft, as an example, trading at a p/e of 30x. While this is a relatively high valuation, it is far from the valuation levels seen during the IT bubble around the year 2000. Bernstein’s analysis, which goes back to 1980, shows no clear correlation that negative equity markets will follow periods with concentrated market advances. In fact, history shows that the subsequent return is only marginally below the normal trend. There is a slightly greater effect on the leading shares, which tend to rise slightly less than the market over the following 6-12 months. They take a breather, so to speak. As always, the key for us is to assess the strategic potential of companies over the long term. AI will probably play a significant role in those assessments.

Risk of Earnings Downgrades

The rapid tightening of monetary policy did a lot of damage in 2022. Going forward, share prices will predominantly be set by the fundamental performance of the individual companies, in our view. Currently, investors are euphoric about AI for a select group of companies – an optimism we, by and large, also share.

One element of uncertainty that can create stock market volatility is the reaction to a possible and quite likely recession in the U.S and other economies around the world. However, a recession might not appear imminent looking at the current growth figures. Still, we know from history that the effects of tighter monetary policy, and especially the effects of the current inverted yield curve, unfold with a delay of approximately 18 months.

“Going forward, share prices will predominantly be set by the fundamental performance of the individual companies, in our view.”

During Q1 2023, the job market responded with a lag of about 18 months during the financial crisis. A recent analysis from J.P. Morgan shows that since mid-2021, the US consumer has spent the extraordinary savings from the period during Covid, corresponding to an amount of approx. USD 1,600 billion. By comparison, annual private consumption in the US is approximately USD 18,000 billion. The reduction in savings has had a significant effect on consumption, but according to the analysis, the excess savings from the Covid period have now been spent, indicating increased private savings and less consumption going forward.

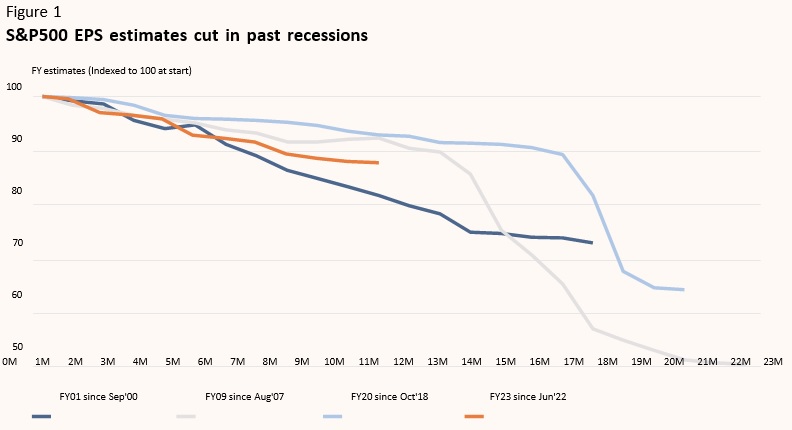

Lower or negative economic growth increases the risk of earnings downgrades. Figure 1 below shows the trajectory of earnings downgrades during previous recessions, and there seems to be a risk of further downgrades if a recession hits.

“From a market perspective, the effect of earnings downgrades is clearly negative. Still, given the significant number of interest rate increases, central banks have now replenished their toolboxes to manage a potential economic downturn.”

Company earnings have increased despite rising cost inflation as companies have been able to raise prices more than cost increases. An analysis from the U.S. Bureau of Economic Analysis (BEA) shows that corporates’ unit margins in the U.S. and earnings per unit of output are at an all-time high. However, going forward, it will be significantly more difficult for companies in general to sustain high prices. It will only be a select group of companies with a strong market position, differentiated products and a high level of innovation that can sustain price increases. One such example is Procter and Gamble, which has a strategic focus on product innovation, giving it a better foundation for raising prices and, thereby potentially higher margins.

Source: Jeffries, March 2023

Central Banks Have Replenished Their Toolboxes

From a market perspective, the effect of earnings downgrades is clearly negative. Still, given the significant number of interest rate increases, central banks have now replenished their toolboxes and are arguably in a better position to manage a potential economic downturn. This is somewhat paradoxical as less than two years ago, the debate was around the extreme monetary policies and consequent negative interest rates that had emptied central banks’ toolboxes with no policy tools left to combat a recession. The key question for equity investors is how quickly central banks will retreat from their hawkish stance as economies weaken. Their rhetoric suggests that they will keep interest rates higher for longer to ensure a solid anchoring of expectation of low inflation. Contrarily, equity investors tend to look forward and start cheering in advance.

Important Information

The views expressed herein may not be reflective of current opinions, are subject to change without prior notice, and should not be considered investment advice.

Performance data shown represents past performance and is no guarantee of future results.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

The price-to-earnings ratio (p/e) is the ratio for valuing a company that measures its current share price relative to its earnings per share (EPS).

FY is an abbreviation for fiscal year.

Earnings per share is calculated as a company's profit divided by the outstanding shares of its common stock.

Unit margin is the difference between the unit price and the unit cost.

Indices listed are unmanaged, and unless otherwise noted, do not reflect fees and expenses and are not available for direct investment.

The MSCI All Country World Index (ACWI) is a stock index designed to track broad global equity-market performance. Maintained by Morgan Stanley Capital International (MSCI), the index comprises the stocks of nearly 3,000 companies from 23 developed countries and 25 emerging markets.

The Dow Jones Industrial Average is a stock market index that tracks 30 large, publicly-owned blue-chip companies trading on the New York Stock Exchange (NYSE) and Nasdaq.

The Nasdaq Composite Index is a market capitalization-weighted index of more than 2,500 stocks listed on the Nasdaq stock exchange. It is a broad index that is heavily weighted toward the important technology sector.

The S&P 500 Index, or Standard & Poor's 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.

3065546