Contact

Contact

March FOMC: The Things Unsaid

March 23, 2023

Executive Summary:

- The Federal Open Market Committee (FOMC) paired a 25-basis point hike with an uncertain path forward in the wake of recent bank failures.

- The market declined from the press conference on, though it was likely more a result of Treasury Secretary Yellen’s dismissal of a broader deposit guarantee than anything Chair Powell said.

- The response is telling as the most important data—what is happening with bank deposits—is hidden from markets and will set the course for the Federal Reserve (Fed).

- The lack of clarity around the banking system and limited upside leaves our defensive positioning intact.

Not Banking on Anything

The Federal Reserve decided to increase interest rates by 25 basis points, while acknowledging the significant uncertainty posed by stress in the banking system. The major changes to the policy statement included a paragraph saying as much about the banking system, dropped the reference to “ongoing increases in the target range,” and acknowledged the recent uptick in inflation. In the Summary of Economic Projections (SEP), the biggest surprise relative to expectations three weeks ago was the year-end 2023 median rate projection, which stayed at one additional hike from here. Before the recent financial turmoil, expectations were for the ’23 dot to increase by 1-2 additional hikes. Obviously, the facts changed so Fed policymakers changed their mind. Ahead of the press conference, the takeaway from the statement and projections was that uncertainty around the outlook continues to increase with each passing meeting.

The press conference largely centered on the strains in the banking system. What is the substitutability of tighter credit conditions and additional rate hikes? Are there more banks at-risk? Won’t further rate increases exacerbate the underlying issues evident in Silicon Valley Bank’s failure that exist in other banks? In response, Powell repeatedly stated that it is too soon to judge the macroeconomic effects, but the Committee’s concern was evident. First off, Powell, on a few occasions, stated that depositors’ savings are safe in the banking system. When pressed on this point, given the Fed’s inability to deliver on this promise on its own accord, Powell noted that the Committee is willing to use its tools towards this end. However, Powell, Treasury Secretary Yellen, and other prudential regulators are playing a confidence game rather than providing policy solutions, which require Congress. It remains to be seen if these promises and slowing deposit churn will be enough to stem the rout in regional banks.

Beyond his insistence that deposits would be protected, the banking strains appear to be worth 1 or 2 additional rate hikes at this point. Powell had comments to that effect and the lack of additional SEP rate increases for 2023 support it as well. The subtext of all the Q&A is what private information is Chair Powell and the Committee revealing about their views on the banking system. Relative to something like forecasting the unemployment rate or inflation, the Federal Reserve can map flows across financial institutions with precision.

The Committee knows what is happening with deposit outflows and inflows across regional and money-center banks. They know who is borrowing from the facilities and they are privy to ongoing negotiations for both recently defunct and teetering institutions alike. I think Powell did his best in talking about the banking system and the Fed’s view in a generic sense, but the contrast between his views and European Central Bank President Lagarde earlier Wednesday is revealing. Whereas Lagarde was emphatic “that there is no trade off between price stability and financial stability,” Powell seemed more circumspect about the Fed’s ability to hike further given recent events. For now, the May FOMC meeting is a toss-up, the economic data says hike, but the health of the banking system may derail it.

Suspended Animation

Caution continues to be the hallmark of our portfolios. The answers we need most: will Congress move forward with any legislation to address the deposit concerns plaguing small banks, is the redistribution of deposits burning out, or are smaller banks’ liquidity needs being addressed at the expense of long-term viability remain elusive. Until we receive more clarity on the banking system, our baseline view is that the odds of a recession in 2023 are high and have increased because of the bank stress. We are underweight equities and prefer quality growth exposures in sectors like communications services. Similarly, our fixed income portfolios are biased to investment grade debt and the front-end of the interest rate curve.

Important Information

The views expressed herein are those of Harbor Capital Advisors, Inc. investment professionals at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice. The information provided in this presentation is for informational purposes only.

This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

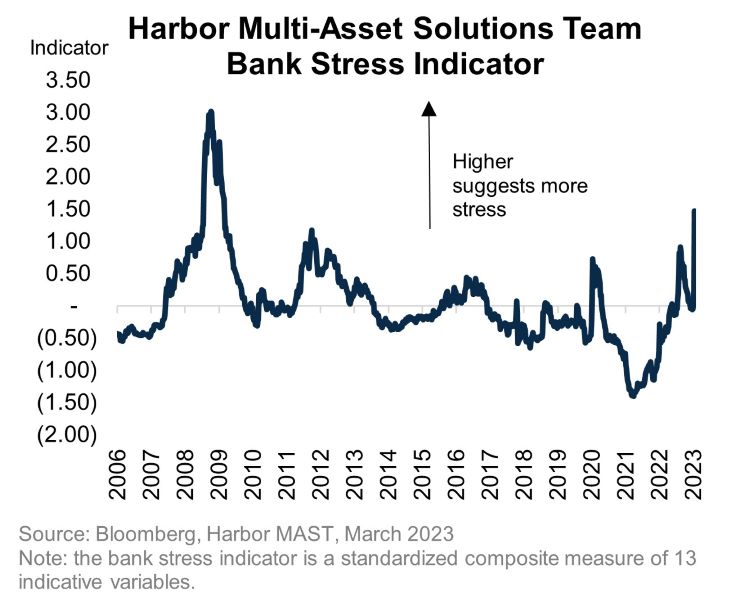

The Bank Stress indicator is intended to provide a singular reading of stress in the banking system by measuring 13 different variables that the Harbor Multi Asset Team views as informative to this end. Each of the 13 variables fall into one of three categories: US Bank Stress (measuring stress with US Banks), International Bank Stress (measuring stress with European Banks), or Growth Activity (measuring economic growth).

Once all 13 variables have been selected and assigned to one of the three categories, each measure is then standardized (Z-scored vs. history) to allow for an apples-to-apples comparison between the variables. A positive/higher standardized score suggests elevated stress for each variable and a negative/lower standardized score suggests low levels of stress. The score for each standardized variable is then averaged within each of the three categories producing three category scores. The three category scores are then averaged to produce an overall Bank Stress Indicator score. This process is repeated each month going back to 2004 to produce a time series of the Bank Stress Indicator scores.

2812498