Contact

Contact

July CPI Brings Temporary Relief

August 18, 2022

Executive Summary

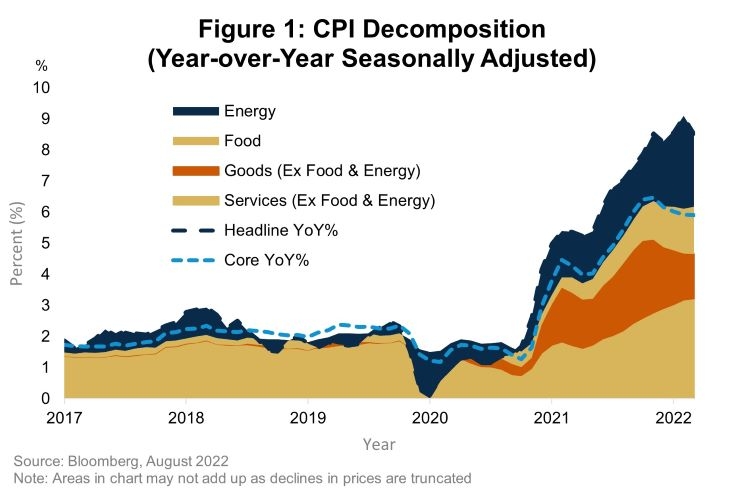

- July Consumer Price Index (CPI) surprised to the downside as headline prices were flat month-over-month, while core inflation decelerated from 0.7 percent to 0.3 percent.

- Falling gasoline prices were the primary contributor to slowing headline inflation as average retail prices declined 13 percent in July.

- Core goods prices also decelerated notably from 0.8 to 0.2 percent month-over-month, a positive sign that healthier supply chains and rising inventories will support lower prices in sectors most adversely affected by the pandemic.

- Despite the positive developments in energy and core goods, services inflation, most importantly housing, remains well above levels consistent with inflation returning to 2 percent on a sustained basis.

- Slower inflation is a relief, but do not forget that the data underscores the difficult task ahead for the Fed to return inflation to target.

Waning Demand and Improving Supply

The decline in energy prices is welcome news for the Federal Open Market Committee (FOMC) and consumers alike as gasoline is one of the most salient prices in the economy. The sharp increase in energy prices has been a major contributor to the deterioration in consumer confidence and the widespread perception that inflation is out of control. The psychology associated with the latter is a critical risk to the Federal Reserve’s (Fed) inflation goals as stable inflation expectations anchor inflation at 2 percent over the longer term. A sustained fall in energy and food prices, another salient consumption category, can offset the strength in core prices to the extent that they play a disproportionate role in how consumers form expectations for prices going forward. Leaving aside core inflation for a moment, it is worth examining what is driving the decline in energy prices.

Global oil supply has improved modestly with draws from the U.S. Strategic Petroleum Reserve accelerating and Russian production remaining near levels that prevailed prior to their invasion of Ukraine. However, the demand picture is eroding. According to the U.S. Department of Energy, implied gasoline demand, on a seasonal basis, is near a 5-year low. Related to lower gasoline demand, the CPI data showed sharp declines in airfare, hotel, and rental car prices. Adding these together, falling energy prices may be more of a reflection of demand destruction for discretionary spending rather than a normalization in global energy markets.

A similar dynamic could be at work in core goods prices, a grouping that includes items like clothes and cars, which decelerated significantly. An improving supply chain is evident in the faster supplier delivery times and lower order backlogs reported in manufacturing surveys. Further confirmation comes from the Federal Reserve Bank of New York’s Global Supply Chain Pressure Index which is at its lowest level since January 2021. At the same time, rising inventories and reported price cuts were a more frequent topic in Q2 earnings calls for several U.S. companies. The bottom line on goods inflation seems to indicate that supply chains are improving significantly and that the excess demand that characterized the initial part of the pandemic is finished.

The Difficult Disinflation Lies Ahead

If the good news on commodities and goods prices continues, the FOMC can turn its focus solely to services inflation, which is the largest portion of the U.S. economy. The July CPI data once again confirmed that the underlying trend in services is inconsistent with 2 percent inflation as shelter prices continue to rise quickly. The question for the FOMC is whether the robust price gains in shelter and other service sectors reflect the explosive demand of 2020 and 2021 or are evidence that aggregate demand remains too high. The answer will dictate the amount of additional tightening from the FOMC.

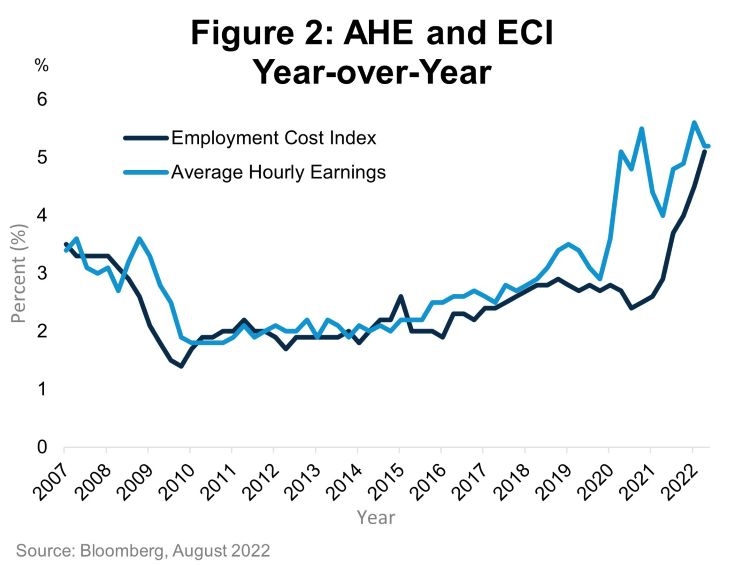

When thinking about aggregate demand and its relationship to inflation, the FOMC relies on the labor market. Tight (loose) labor markets result in increasing (decreasing) wages, which are then reflected in prices. The July Employment Situation Report and other wage data over the past few weeks suggests that the labor market remains too tight. Average hourly earnings and the employment cost index are increasing at year-over-year rates above 5 percent, at the same time productivity measures have slowed significantly. The FOMC will view robust wage gains and dwindling productivity as a sign that the labor market is past full employment.

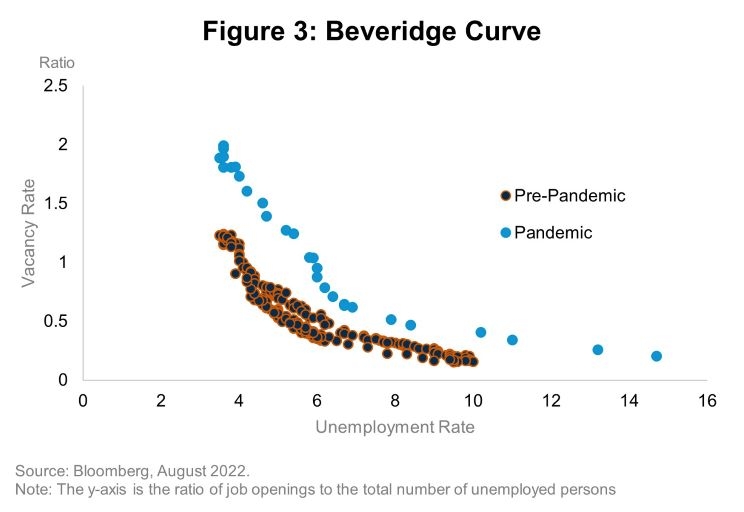

The policy debate going forward will center around what a looser labor market will look like in practice, not whether it is necessary. Chair Powell and other members of the Committee have argued that excesses in the labor market are most apparent in job postings and the elevated quits rate where an adjustment to more sustainable levels may not have a significant impact on the unemployment rate. However, the historical record indicates that similar declines in job vacancies and the quits rate are consistent with unemployment increasing to a higher level than the 4.1 percent outlined in the FOMC’s June projections. The upshot of all of this is that we continue to expect the unemployment rate to increase materially from here as we agree that the labor market remains too tight.

Still Clinging to Safety Despite Better News

The July CPI does not change our core thesis that continued Fed tightening and the resultant rise in unemployment will lead to poor risk asset returns going forward, but it does increase the probability of a soft landing somewhat. We remain overweight fixed income, particularly Treasuries and Agency mortgage-backed securities. However, investment grade credit is increasingly attractive as corporate earnings underscored the durability of highly rated firms’ business models and steady issuance has led to a modest underperformance of investment grade credit relative to lower-rated debt. We continue to believe that high yield is unattractive at current spread levels, which have been supported by the recent outperformance of risk assets and a significant contraction in outstanding supply. In equites, healthcare remains our highest conviction sector, and we prefer higher quality, more profitable factor exposures.

For more information, please access our website at www.harborcapital.com or contact us at 1-866-313-5549.

Important Information

The views expressed herein are those of Harbor Capital Advisors, Inc. investment professionals at the time the comments were made. They may not be reflective of their current opinions, are subject to change without prior notice, and should not be considered investment advice. The information provided in this presentation is for informational purposes only.

This material does not constitute investment advice and should not be viewed as a current or past recommendation or a solicitation of an offer to buy or sell any securities or to adopt any investment strategy.

Performance data shown represents past performance and is no guarantee of future results.

Investing entails risks and there can be no assurance that any investment will achieve profits or avoid incurring losses.

2381443